Updated: 02 December 2025

Gifting money to children in 2026: at a glance

- What do I need to know? Young people are saving more money than ever, but still struggle to build financial resilience.

- What does it mean for me? More parents and guardians than ever are gifting money to children earlier to help out, setting aside an average of £18,212 for dependents in the UK.

- Why does it matter? The earlier you gift, the less likely you’ll pay high levels of tax, keeping more of your money with loved ones.

Research commissioned by Flagstone shows that 61% of younger people (aged 18-34) keep at least three months’ salary for emergencies.

Despite this, younger generations are still struggling financially, and parents are turning to early inheritances to help. The ‘great wealth transfer’ is projected to pass down as much as £7tn over the next 30 years in the UK alone.

There are several ways to transfer wealth between generations without paying unnecessary tax. Understanding the rules means that you can make the best decisions for your finances, ensuring that the money you gift stays in the family.

But making sense of the guidance is a challenge. The combination of exemptions, allowances, and lesser-known HMRC rules can make it difficult to know how much money you can gift tax free. Additionally, the amount you plan to save for your children could vary depending on where you live in the UK.

In this article, you’ll learn how to gift money to children in the most tax-efficient way possible in the current tax year. You’ll also discover the average amount each region of the UK is planning to gift to children, and where most parents in the UK expect their children to spend the savings they receive.

How gifting money to family works in the UK

In the UK, the rules around gifting money to family vary depending on who gets the gift and the size of your donation. If the gift is taxable, the giver is the one who needs to pay, not the person receiving it.

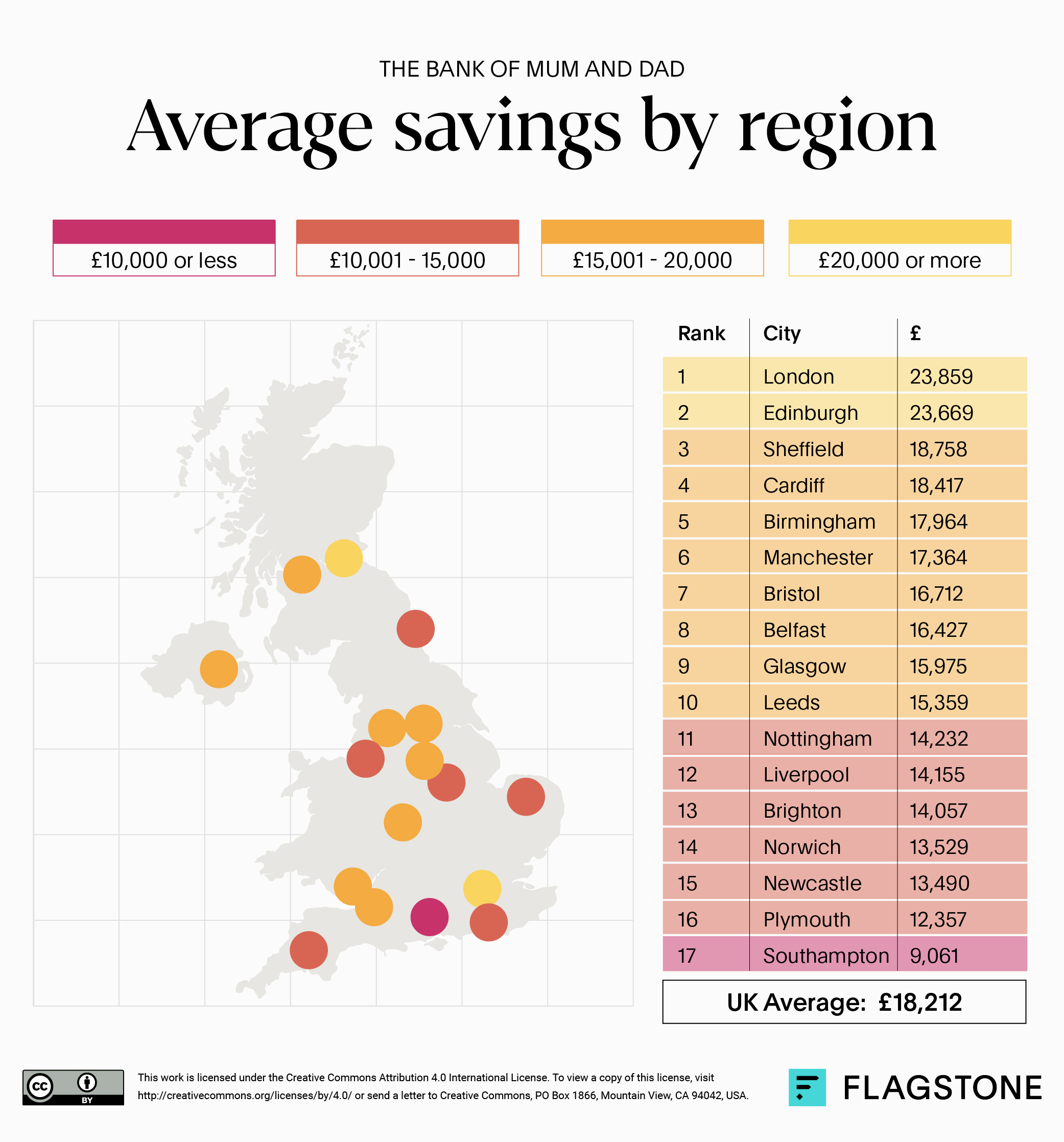

How much does each region of the UK plan to gift to their children?

Flagstone’s research identified significant geographic variations in the amount of money parents plan to gift to their children. Our research shows the highest average savings by region were in London and Edinburgh, at around £26,500.

The city that saves the least for their children according to the research is Southampton, with an average parental saving of £9,061.24.

Gifting money to children vs. spouses

Partners and spouses are exempt from Inheritance Tax (IHT), meaning there are no limits on what they can receive.

But children aren’t exempt, which means they could face tax charges depending on the amount gifted (more on that later). We’ve listed five ways you can reduce tax bills when passing on your wealth.

Five methods for gifting money to children in the UK tax-free

1. Annual exemption

The annual exemption means that every year, you can donate £3,000 without paying tax. The allowance is given to each taxpayer, so two parents can give £3,000 respectively. This means that you could pass on £6,000 tax-free if you both choose to make a gift .

You can carry over your annual exemption to the following tax year if you haven’t used it. But you can only do this once.

| Pro | Con |

| You can pass money on easily. | Both parents need to contribute to maximise the donation. |

2. Small gift allowance

You can gift up to £250 each year to as many people as you like without paying tax, as long as you haven’t used another allowance (like the annual exemption) for the same person in that tax year.

| Pro | Con |

| It applies to as many people as you like. | The allowance is small. |

3. Wedding or civil partnership gifts

You can gift as much as £5,000 tax-free to a child if they’re getting married, or entering a civil partnership. The limit for grandchildren or great-grandchildren is £2,500. If you want to gift wedding money to anyone else, you can donate up to £1,000.

| Pro | Con |

| Your children can receive a significant, tax-free lump sum. | It depends on whether your children get married. |

4. Normal expenditure out of income

This lesser-known rule means you can pay for children’s costs out of your own income tax-free. This can include paying rent, or contributing to a savings account for children under 18.

You can only use the ‘normal expenditure out of income’ rule if it won’t affect your quality of life. There’s no limit on contributions, but payments must be made regularly from your income.

| Pro | Con |

| There’s no limit to what you can contribute. | Payments must be regular. |

5. Early inheritance

Your loved ones won’t pay Inheritance Tax on gifts you give during your lifetime. Instead, the government takes tax out of your estate (everything you own) when you pass away. Every UK taxpayer can transfer an allowance of £325,000 tax-free. If the total value of your estate is below £325,000, your beneficiaries won’t pay Inheritance Tax.

If your estate is worth more than this allowance, you may have to pay Inheritance Tax. But if you’re gifting money to children early, there’s a higher chance your gift will become exempt. This is because of the seven-year rule.

| Pro | Con |

| You can gift large amounts of money to your children. | You could pay Inheritance Tax if you pass away unexpectedly. |

What is the seven-year Inheritance Tax rule?

The seven-year rule means that gifts you make during your lifetime may be subject to Inheritance Tax if you pass away within seven years. But the longer you live after making a gift, the less tax may be due. If you live for seven years or more, your gift becomes exempt from Inheritance Tax, and won’t be included in your estate.

Here’s how it works:

| Years between gifting and passing away | Inheritance Tax rate |

| Up to three years | 40% |

| 3-4 years | 32% |

| 4-5 years | 24% |

| 5-6 years | 16% |

| 6-7 years | 8% |

| Seven years or more | 0% |

How much money can you gift tax-free to a family member in the UK?

If two parents use their annual exemption, and carry over their allowance from the year before, they can contribute £6,000 each. If this goes to one child, that would mean they can give £12,000 tax-free. This means you could gift as much as £12,000 in a year without it being counted as part of your estate.

Your circumstances will be unique, so it’s important to get professional advice. Speaking with a Financial Adviser can help you if you’re unsure how to maximise your tax efficiency.

Gifting money to adult children vs. gifting property

Adult children (18 years old and above) can receive different kinds of gifts, including property.

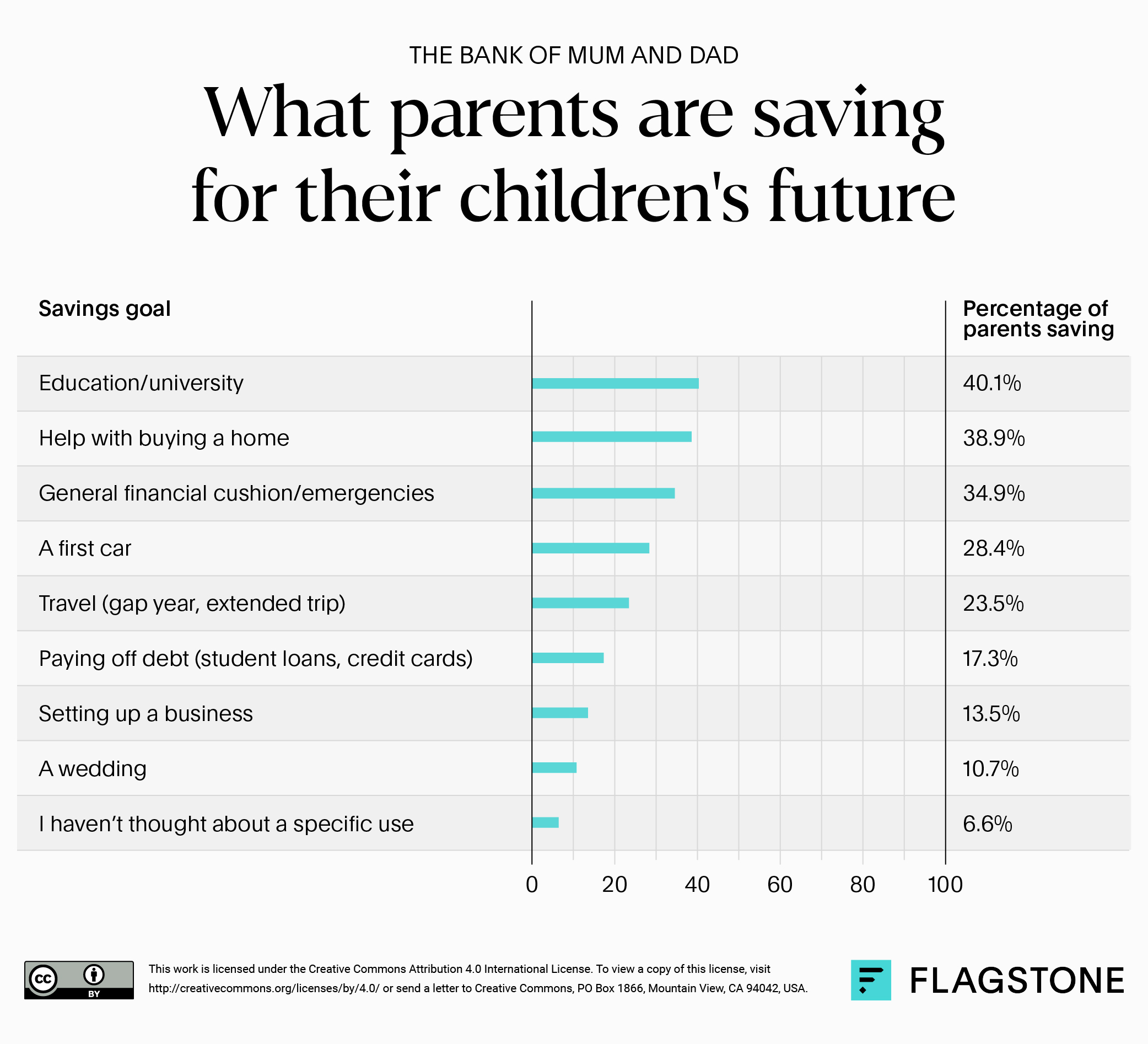

According to Flagstone’s 2025 survey, as many as 38.9% of parents that are planning to gift money to children listed ‘help with buying a home’ as a savings goal.

This suggests that a significant number of parents plan to use cash savings to get their children on the property ladder, rather than passing on property directly.

There are a handful of reasons why this might be the case.

Estates are based on value

Property can quickly use up your Inheritance Tax allowance if you don’t pass it on to a husband, wife, or civil partner who are exempt.

If you pass on property to a child, or grandchild, and your estate is worth less than £2m, your tax-free threshold can increase to £500,000. The seven-year rule also applies to property, so if you pass away unexpectedly within seven years, your child might need to sell the property to cover any Inheritance Tax.

If an adult child sells a property you’ve gifted, they could be responsible for paying Capital Gains Tax on the profit they make from the sale.

Gifting money to younger children

In addition to the methods above, you can give money to younger children (under 18 years old) if they have a Junior ISA (or JISA). Parents and grandparents can pay into an account on their behalf. The limit for contributions into a JISA is £9,000 per tax year, per child.

Setting up trusts

Trusts can give you control over the circumstances of payments, making them an attractive tool for gifting money. Trusts involve three people, known as the:

- Settlor: The person paying into the trust (you)

- Trustee: The person managing the trust (someone you nominate over the age of 18)

- Beneficiary: The person benefitting from the trust (your child, grandchild, or another person you choose)

Tax rules can be complex for trusts, so it’s important to consider whether an early inheritance is a more efficient option.

Frequently asked questions on gifting money to children

Can I gift £3,000 to each child in the UK?

No, your allowance is a set amount you can donate annually. But you can split your gift between multiple people. For example, three children could receive £1,000 each from one parent.

Can I give my son £20,000?

Yes, you can gift as much money as you like. But depending on the circumstances you may have to pay tax on some of the donation. For larger gifts, it may be a good idea to give earlier. This increases your chances of not paying Inheritance Tax, as gifts made seven years before you pass away are exempt.

Do I need to declare cash gifts to HMRC in the UK?

No, you would only need to report it to HMRC if the cash gift resulted in dividends or interest. This is because dividends and interest are considered income unless earned in an ISA.

Gifting money to help children build future wealth

Gifting money to family, especially children, can help set your loved ones up for future success despite the financial challenges they face.

Combining multiple forms of tax relief minimises what you need to pay. But it’s worth speaking to a qualified professional to ensure you’re following the rules.

For parents looking to pass on their wealth to younger generations, using the right tools can help spread risk and maximise earnings across a diversified portfolio.

With strong finances, you’ll be in the best position make an impact with your generosity.

Generate a personal illustration to see what you can earn

Open multiple savings accounts to build your earning potential with Flagstone.

Access hundreds of accounts from 65+ banks.

Use the calculator below to discover what you could earn.